Welcome to the intricate maze that is cryptocurrency taxation! If you've dabbled in the world of digital assets, you know that the tax implications can be as volatile as the market itself.

Navigating the tax landscape is crucial for any savvy crypto investor. After all, the last thing you want is to watch your hard-earned gains get eroded by hefty tax bills.

That's where this guide comes in. We aim to arm you with legal strategies to minimize your tax liability, helping you keep more of what you earn.

Let’s show you how to avoid capital gains taxes on crypto!

We've laid out some key strategies that should help most individuals and have also provided some unique strategies available depending on which country you are declaring in.

In the following sections, we'll delve into various tactics like holding your assets, tax loss harvesting, leveraging losses and some common myths !

We’ll start of with advice most relevant for those in the USA and then discuss country-specific advice for those residing in Sweden, Germany, Finland, Portugal, or Japan. If you're in another country, do not worry. Look into our tax guides for our supported countries, where we cover tax systems in more depth.

Understanding Tax Events

Let's start by laying the groundwork: What exactly is a taxable event in the realm of cryptocurrency? Understanding this is key because not all crypto activities are taxed equally or even at all.

A taxable event is essentially any transaction that results in a tax liability. In the crypto world, these events can be more varied than you might think.

Selling Cryptocurrency for Fiat

This one might seem obvious. When you sell your cryptocurrency for fiat money, like dollars or euros, you're realizing a gain or loss. This is a taxable event, and the rate at which you're taxed could depend on how long you've held the asset.

Even if you keep the fiat on an exchange and do not send it to your bank account, selling crypto for fiat remains taxable.

Trading One Cryptocurrency for Another

Believe it or not, swapping Bitcoin for Ethereum or any other crypto-to-crypto trade is a taxable event. You're required to calculate the gain or loss in the value of the asset you're giving up, and you'll be taxed accordingly.

Using Cryptocurrency for Goods and Services

Spending cryptocurrency is seen the same as selling it and is, therefore a taxable event. If you use Bitcoin to buy a laptop, for instance, you'll need to calculate the gain or loss on the Bitcoin you spent.

Staking

When you stake your cryptocurrency, the rewards you receive are considered income and are therefore taxable. This is true even if you reinvest those rewards.

Mining

Mining cryptocurrency isn't just a way to earn tokens; it's also a taxable event. The IRS, for example, considers mined crypto to be income, and it becomes subject to income tax.

Liquidity Pools

Participating in a liquidity pool? The fees you earn are considered income and are taxable. Additionally, when you remove your assets from the pool, you'll need to account for any capital gains or losses.

Depending on your country simply moving crypto to a defi platform may be a taxable event!

Understanding these taxable events is the first step in smart crypto tax planning. Armed with this knowledge, you can make more informed decisions that could legally minimize your tax liability.

Holding as a Long-term Capital gain Strategy

You've probably heard the term "HODL" thrown around in crypto circles. It's more than just a meme; it's a tax-efficient strategy.

Holding your cryptocurrency for the long term can offer significant tax advantages. In many jurisdictions, long-term capital gains are taxed at a lower rate than short-term gains.

So, what qualifies as "long-term"?

In the United States, for example, holding an asset for more than one year moves it into the long-term capital gains category. The rates for these gains can be substantially lower than those for short-term gains, which are taxed as ordinary income.

2023 Long-Term Capital Gains Tax Brackets

| Tax Bracket/Rate | Single | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 0% | $0 - $44,625 | $0 - $89,250 | $0 - $59,750 |

| 15% | $44,626 - $492,300 | $89,251 - $553,850 | $59,751 - $523,750 |

| 20% | $492,301+ | $553,851+ | $523,751+ |

But it's not just about the U.S. Different countries have their own rules on long-term gains.

For instance, in Germany, if you hold your cryptocurrency for more than one year, the gains are tax-free.

However, this strategy isn't without its risks. The volatile nature of cryptocurrency markets means that holding long-term could expose you to downturns.

That's why it's crucial to weigh the potential tax benefits against the market risks.

How Crypto Gifts Can Avoid Crypto Taxes

Gifting your crypto assets to family or friends can be a win-win for both parties involved. Not only do you avoid recognizing any capital gains, but the recipient also doesn't have to treat it as income.

Making charitable contributions to qualified organizations can also allow for deductions.

But how do gifts lower your taxes?

Gifting Crypto to Individuals

When you gift cryptocurrency, the IRS generally doesn't require you to pay taxes on the transaction. The catch? The value of the gifted crypto must be below the annual gift limit, which is $17,000 for the year 2023.

If the value exceeds this limit, you'll need to file a gift tax return. However, you may still not owe any taxes if you haven't hit your lifetime limit of $12.92 million for 2023. Any amount over the annual limit will reduce your lifetime exemption.

Receiving Crypto as a Gift

On the flip side, if you're the lucky recipient of a crypto gift, you also won't owe any taxes on it. The IRS doesn't view it as income.

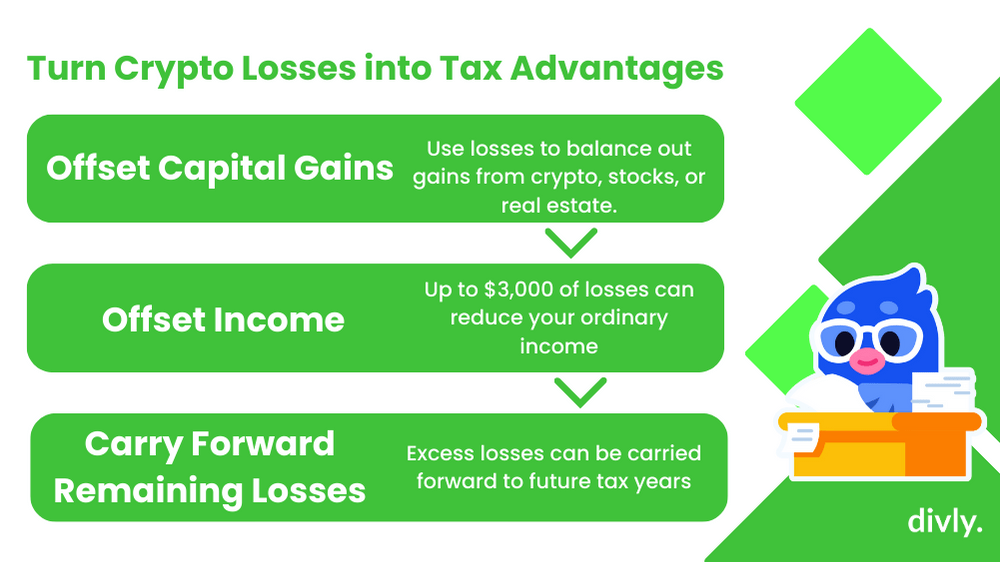

Leveraging Your Losses To Avoid Crypto Capital Gains Taxes

Cryptocurrency investments can be volatile, and losses are a part of the game. But did you know that these losses can actually work in your favor come tax time?

Offset Capital Gains

If you've incurred capital losses in your crypto investments, you can use these to offset any capital gains you might have. This applies not just to gains from other cryptocurrencies but also to gains from other types of investments like stocks or real estate.

In essence, your losses can help reduce your overall tax liability.

Offset Ordinary Income

But what if you don't have any capital gains to offset? The IRS allows you to use up to $3,000 of your capital losses to offset your ordinary income if you're filing as a single taxpayer.

This means that even if you don't have capital gains, you can still benefit by reducing your taxable income for the year.

Carry Forward Losses

If your losses exceed the $3,000 limit, don't worry. You can carry forward these losses into future tax years. This means that if you have a particularly bad investment year, the silver lining is that you can use those losses to offset gains or income in the years to come.

Strategic Planning

Interestingly, you might not want to use the full $3,000 allowance in a single year. If you anticipate higher income or more substantial capital gains in the future, saving some of your allowable losses for those years could be a strategic move.

Tax Loss Harvesting To Lower Your Crypto Tax Bill

In the world of cryptocurrency trading, not every investment is going to be a winner. While it's great to ride the highs, it's equally important to have a strategy for the lows.

One such strategy, particularly relevant for U.S. investors, is selling cryptocurrencies that are performing poorly to offset gains made from other investments. This is commonly known as "tax-loss harvesting."

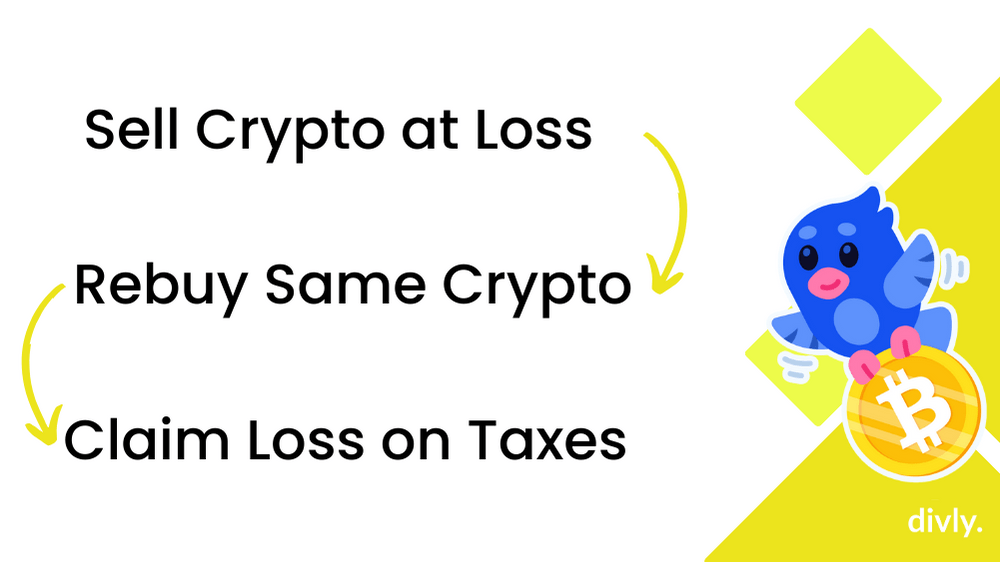

Utilize Wash Sales While You Still Can

One strategy has stood out for its ability to offset gains: wash sales. Unlike traditional investments in stocks and bonds, cryptocurrencies are currently not subject to wash-sale rules!

What does this mean for you?

Well, you can sell your cryptocurrency at a loss and buy it right back, recognizing that loss on your tax return to offset other gains. This allows you to essentially maintain the same position in your crypto investment while taking advantage of the tax benefits.

However, this tax loophole may soon be closing.

In President Biden's fiscal 2024 budget proposal, a change has been suggested to align the tax treatment of cryptocurrencies with that of stocks and bonds. If this change is enacted, wash-sale rules would also apply to cryptocurrencies.

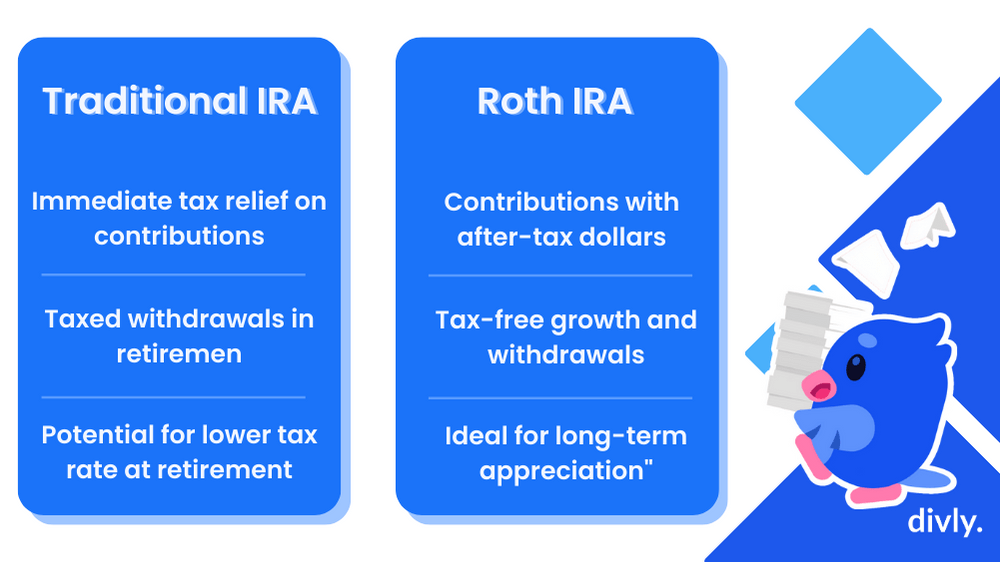

Retirement Accounts Can Save You On Crypto Taxes

When it comes to managing your crypto assets, thinking long-term can pay off—especially when you consider tax-deferred retirement accounts like Traditional IRAs and Roth IRAs.

So, what's the deal with these accounts?

Traditional IRA: Immediate Tax Benefits

Investing your cryptocurrency in a Traditional IRA can offer immediate tax relief. Contributions to this account are often tax-deductible, meaning you could lower your taxable income for the year you make the investment.

However, it's essential to remember that withdrawals from a Traditional IRA are taxed as income. The silver lining? By the time you reach retirement, your tax rate could be significantly lower than it is today.

Roth IRA: Tax-Free Growth and Withdrawals

On the other hand, a Roth IRA offers a different kind of tax advantage. While contributions to a Roth IRA are made with after-tax dollars—meaning no immediate tax deduction—the investment grows tax-free.

Even better? You can make withdrawals from a Roth IRA tax-free, provided you meet certain conditions. This can be a huge benefit if you expect your crypto investments to appreciate substantially over time.

Know the Limits

Both Traditional and Roth IRAs come with their own set of rules, including contribution limits and conditions for tax-free withdrawals. It's crucial to familiarize yourself with these details to maximize the tax benefits.

Misconceptions about Crypto Taxes

Can I avoid Taxes by using Cryptocurrency?

A prevalent misconception is that cryptocurrencies are a way to evade taxes. In reality, many countries, including the United States, treat cryptocurrencies like any other form of property for tax purposes, meaning gains from crypto transactions are subject to capital gains tax.

Are Only Crypto-to-Cash Conversions Taxable?

No .tax liabilities also arise from other types of transactions, such as trading one cryptocurrency for another, using cryptocurrency to purchase goods or services, or earning cryptocurrency through mining or staking.

Does Anonymity in Transactions Means Anonymity from Taxes?

This is a very worrisome misconception. Not only could you subject yourself to penalties, but crypto transactions are less anonymous than you think. Blockchain technology allows for a public ledger of all your transactions. Companies like Chainalysis specialize in tracking those transactions and working with authorities to catch fraud and tax cheats

Lowering Crypto Taxes in Sweden

For more comprehensive information see our guide on optimizing crypto taxes in Sweden.

Declare Your Crypto Losses to Skatteverket

Firstly, it's essential to declare your crypto losses to Skatteverket, the Swedish Tax Agency. By doing so, you can offset 70% of your losses against profits from crypto or other assets like stocks.

If you find yourself with a deficit (SV: underskott), these losses can also be used to reduce your income tax. Remember, failing to declare your taxes is a criminal offense in Sweden, so compliance is crucial.

Timing of Calculating Your Losses

The deadline for declaring your taxes in Sweden is in May. However, it's beneficial to keep track of your profits and losses throughout the year.

By staying updated, you can use this information strategically to help minimize your taxes.

How Crypto Losses Can Lower Your Taxes

Crypto losses can have a multi-faceted impact on your tax situation. They can decrease your capital gains taxes, interest income taxes, and even income taxes in some cases.

Calculating and tracking these can be complex, but tax calculators like Divly can simplify the process.

Using Losses to Offset Profits and Interest Income

In Sweden, you can use 70% of your crypto losses to offset your crypto profits. For example, for every 10 SEK of losses, you can deduct 7 SEK from your crypto profits when calculating your taxes.

Additionally, staking rewards and crypto interest are subject to a 30% interest income tax. You can use 70% of your crypto losses to offset this interest income tax as well.

Offsetting Losses in Other Assets

Your crypto losses can also be used to offset gains from various sections in your Swedish tax declaration. These sections include profits from stocks, real estate, and other types of assets.

Using Losses from Other Assets to Lower Crypto Taxes

Conversely, losses from other assets can be used to lower your crypto taxes. For example, losses from stocks can be used to reduce your crypto capital gains tax by 70%.

Deficits and Income Tax Reduction

If your losses exceed your income from capital gains, it's called a deficit (SV: Underskott). A deficit up to 100,000 SEK can grant a 30% tax reduction from your state and municipal tax. Deficits over 100,000 SEK can be granted a 21% tax reduction.

Avoiding Crypto Taxes in Germany

€600 Exemption Limit on Crypto Profits

In Germany, you enjoy a €600 exemption limit on profits made from private sales transactions, which include not just cryptocurrencies but also other assets like art or cars.

If your profits are under €600 for the year, you won't have to pay any taxes on them. However, it's essential to note that if you exceed this limit, taxes are due on the entire amount, not just the excess over €600.

You can also carry forward losses to offset future gains on private sales transactions, providing another avenue for tax optimization.

If you know you are just barely over this limit it may help to sell some crypto at a loss to get back under the €600 limit.

12-Month Holding Period

One of the most significant tax benefits in Germany is the 12-month holding period.

If you hold your cryptocurrency for more than a year, you are exempt from paying any taxes on the gains you realize upon selling them. This long-term holding strategy can be particularly beneficial for those looking to invest in crypto as a long-term asset.

€256 Exemption Limit on Crypto Income

Income from other crypto-related services like mining, staking, and airdrops also enjoys a tax exemption, but the limit here is €256 per year.

If your income from these services exceeds €256, you'll have to pay taxes on the entire amount, similar to the rule for crypto profits.

Lowering Crypto Taxes in Finland

Navigating the Finnish crypto tax landscape can be a bit of a maze, but there are several strategies to legally minimize your tax burden. Here's how:

Utilize the Deemed Acquisition Cost to lower your taxes

In Finland, one of the most effective ways to lower your crypto taxes is by using the deemed acquisition cost. This rule allows you to deduct either the actual or the deemed acquisition costs from the selling price of your crypto assets.

The deemed acquisition cost is set at a minimum of 20% of the sale price if you've held the asset for less than ten years. This percentage jumps to 40% if you've held the asset for a decade or more.

This is particularly beneficial for volatile assets like cryptocurrencies, where the actual acquisition cost might be significantly lower than the deemed acquisition cost. For example, if you bought 1 BTC for €1,020 and sold it for €20,000, using the deemed acquisition cost of 20% (€4,000) would reduce your taxable profits to €16,000, saving you €2,980 in taxable profits.

Divly’s tax platform is the only tax platform for cryptocurrencies that uses the deemed acquisition cost to lower your taxes!

Using the Deemed Acquisition Cost for Smaller Cryptocurrencies

The deemed acquisition cost is also useful if you can't find pricing information for one of your cryptocurrencies. This is especially beneficial for smaller cryptocurrencies where pricing information might not be readily available.

Can You Offset Losses?

Yes, you can offset losses made on cryptocurrency trading. According to [§ 50 of the Income Tax Act)(https://www.finlex.fi/fi/laki/ajantasa/1992/19921535#O3L2P50) in Finland, selling your cryptocurrencies at a loss is tax-deductible as long as the total sales prices are over €1,000.

You can deduct these losses from your gains on the sales of other virtual currencies in the same tax year and the five subsequent years. However, it's crucial to note that you can only deduct losses if you've actually sold your cryptocurrencies. If your assets have decreased in value but you still own them, you can't deduct any losses.

Lowering Crypto Taxes in Portugal

Portugal has a unique stance on cryptocurrency taxation, offering several avenues for traders and investors to minimize their tax liability. Here's how you can navigate the Portuguese crypto tax landscape effectively.

Long-Term Holding Benefits

One of the most straightforward ways to avoid capital gains tax on your crypto assets in Portugal is by holding them for at least 365 days. According to Article 19 of the Personal Income Tax Code, gains and losses from transactions involving crypto assets held for a period equal to or longer than 365 days are not taxable.

Crypto-to-Crypto Transactions

Article 20 states that if you exchange one cryptocurrency for another, the transaction is not subject to taxation. The newly acquired crypto assets are assigned the acquisition value of the delivered crypto assets. This means that you can strategically trade between cryptocurrencies without triggering a taxable event.

Taking Advantage of the FIFO Method for Multiple Wallets in Portugal

In Portugal, the First-In-First-Out (FIFO) method is the mandated approach for calculating gains or losses on your cryptocurrency transactions.

What makes this particularly interesting is that the FIFO method must be applied separately for each wallet you own. This opens up some strategic avenues for minimizing your tax liability.

The Advantage of Multiple Wallets

By keeping multiple wallets, you can segregate your crypto assets based on their acquisition cost. For instance, you could have one wallet containing Bitcoin bought at lower prices and another wallet containing Bitcoin bought at higher prices.

When it comes time to sell, you can choose to sell from the wallet containing Bitcoin with a higher acquisition cost. By doing so, the difference between your selling price and acquisition cost—your capital gain—will be smaller, thereby reducing the amount on which you'd owe taxes.

Loss Deduction Limitations

Be cautious when trading with counterparties in countries with favorable tax regimes. According to Article 63-D and Article 55, losses may not be deductible if the counterparty is subject to a tax regime in a country with a tax rate 60% lower than Portugal's.

On P2P exchanges you may not know who you are selling to making it unclear if you can deduct your losses.

However, you can carry forward losses for up to 5 years.

Lowering Crypto Taxes in Japan

For more information see our comprehensive guide on lowering your crypto taxes in Japan.

Japan has a well-defined regulatory framework for cryptocurrency taxation, enforced by the National Tax Authority (NTA). If you're a crypto trader in Japan, it's crucial to understand how to minimize your tax liability. Here are the seven best ways to achieve cryptocurrency tax savings in Japan:

Selecting the Best Cost Basis Method

In Japan, you can choose between the Total Average Method and the Moving Average Method to determine the acquisition cost of your sold cryptocurrencies. The method you choose can significantly impact your taxes. Generally, the higher the acquisition cost, the lower your taxable profits.

-

Moving Average Method: This method calculates the average cost of all the crypto of the same type you currently own. Each time you acquire new crypto, the average price is updated.

-

Total Average Method: This method considers all previous acquisitions and any acquisitions in the current year to calculate the average cost.

Tip: Use a cryptocurrency tax calculator like Divly to test both methods and see which one minimizes your tax liability.

Deducting Necessary Expenses

You can deduct expenses directly related to your cryptocurrency trading, such as:

-

Trading fees

-

Internet and smartphone usage fees

-

Costs of personal computers used for trading

These deductions can lower your overall taxable income.

Using the Deemed Acquisition Cost

In Japan, you can set the acquisition cost of a sold cryptocurrency to 5% of the sale price. This is particularly useful if you've forgotten the purchase price or if the crypto has significantly appreciated.

Offsetting Losses within Miscellaneous Income

You can offset miscellaneous income gains with losses from miscellaneous income. However, you can't offset these losses against other types of income like salary or business income.