Welcome to our guide on crypto taxes in Estonia. When writing this guide, we reviewed all of the applicable regulations, and for any questions that remained, we contacted the Estonian Tax and Customs Board (EMTA) to clarify some key parts that should help clarify how you should declare your taxes.

So, what are we going to cover in this guide?

-

When you should declare your crypto

-

How your cryptocurrencies are taxed

-

Deep dive into each transaction type and its tax consequences

-

How to submit your tax report to the EMTA

Finally, the FAQ, including the answer on everybody’s mind: “How do I lower my crypto taxes?”

This guide is updated and maintained on a regular basis to account for changes made by the EMTA and for new types of transactions. In the event that you find any errors or outdated information, it is greatly appreciated if you let us know by sending an email to [email protected].

When should you declare your cryptocurrencies?

-

15 February 2026 - Online tax portal opens, and you can start declaring your taxes.

-

30 April 2026 - Last day to submit your taxes

Each April, you will have to declare your income from transactions that occurred in the previous calendar year.

How is crypto taxed in Estonia?

In Estonia, cryptocurrency income is considered gains from the transfer of property and is subject to a 20% income tax rate. All profitable transactions must be declared regardless of the amount of profit incurred.

Any of the following transactions can result in cryptocurrency income

-

Sell Crypto

-

Trade Crypto to Crypto

-

Purchase Goods & Services with Crypto

-

Sell cryptocurrency that was mined

-

Earn Staking rewards

-

Earn crypto interest

-

Receive wages in cryptocurrency

-

Pay network fees in cryptocurrency

-

Buying NFTs with cryptocurrency

-

Selling NFTs

We’ll go into a little more depth on how the income for each of these transactions is calculated and declared just a bit later in this guide. A crypto tax calculator made for Estonia, such as Divly, will automatically calculate your income from these transactions for you and guide you through the declaration process.

Some transaction types will not result in a taxable transaction, such as:

-

Buying cryptocurrency

-

Donating cryptocurrency

-

Transferring cryptocurrencies between your wallets/exchanges

-

Gifting cryptocurrencies

How to Calculate your Gain or Loss on Trading Cryptocurrency

To calculate your gains you have to deduct the purchase price (including fees) from the sale price. Determining the purchase price may not be easy. The EMTA themselves say “...it is difficult to keep records of the acquisition cost of each individual cryptocurrency” Therefore they allow for two methods of determining which cryptocurrency you are selling. These are the FIFO (First-in, First-out) method and the Average Cost Method.

The FIFO method assumes that cryptocurrencies are sold in the order in which they were acquired. So, when you sell a cryptocurrency such as Ethereum, you can assume that the Ethereum you are selling is the first one that you acquired.

Example: FIFO

Say you have made the following transactions

| Date | Type | Amount | Price |

|---|---|---|---|

| January 15th | Purchase | 1 ETH | 1000 EUR |

| February 15th | Purchase | 1 ETH | 500 EUR |

| March 15th | Sell | 1 ETH | 2000 EUR |

To determine which Ethereum was sold on March 15th, we’d look at the order of our acquisitions. In this case we can see that the first time we purchased Ethereum was on January 15th, and thus we assume that this is the Ethereum we sold on March 15th.

Note that all profits, no matter how small, must be declared. The EMTA even says the following:

“If gains of 1-2 cents have been generated from the sale of cryptocurrency, should the transaction be declared in the income tax return? Yes, all profitable transactions must be declared in the income tax return”

Example: FIFO involving multiple sales

In this example, we’re going to make things a bit more difficult, do not worry if it’s a little hard to follow. At the end of the day, if you have a tax calculator you won’t have to worry about this anyway

| Date | Type | Amount | Price |

|---|---|---|---|

| January 15th | Purchase | 1 ETH | 1000 EUR |

| February 15th | Purchase | 1 BTC | 10000 EUR |

| March 15th | Sell | 0.5 ETH | 501 EUR |

| April 15th | Sell | 1 BTC | 3 ETH (valued at 12000 EUR) |

| May 15th | Sell | 1 ETH | 6000 EUR |

We’ll only look at the sales of ethereum In this example. Although I can quickly tell you that the sale of BTC resulted in a 2000 EUR gain.

Ethereum's first sale happened on March 15th, where 0.5 ETH was sold for 501 EUR. This sale is supported by our initial acquisition of Ethereum on January 15th, where we bought 1 ETH for 1000 EUR. Selling half of this ETH for 501 EUR, we originally paid 500 EUR for this 0.5 ETH. This means we made a small profit of 1 EUR.

After this transaction, we're left with 0.5 ETH, valued at 500 EUR.

The next Ethereum sale occurs on May 15th, selling 1 ETH for 3000 EUR. At this point, we only have 0.5 ETH left from the January purchase.

Since this doesn't cover the full amount being sold, we also consider our next Ethereum acquisition. On April 15th, we traded 1 BTC for 3 ETH, valued at 12000 EUR, meaning each ETH was acquired at 4000 EUR. Thus, selling 0.5 ETH from this acquisition equates to 2000 EUR.

Therefore, in the May sale, we are essentially selling 0.5 ETH from January (acquired for 500 EUR) and 0.5 ETH from April (acquired for 2000 EUR), totaling 2500 EUR in cost against a sale price of 3000 EUR. This results in a taxable profit of 500 EUR.

Can I use my crypto losses to offset my gains?

Section 39 of the Income Tax Act allows losses from securities to be deducted from gains from securities. As cryptocurrency is not considered a security, this privilege does not extend to it. Therefore, you cannot currently deduct your losses from cryptocurrency trading from your profits.

This means that you will only have to report profitable transactions, and loss-making transactions can be completely ignored.

However, we're left with a question here, which we asked EMTA for clarification on. If I sell all of my cryptocurrency at once, even though they were acquired over multiple transactions, can I consider this as one trade, or do I have to calculate the gain/loss for each acquisition separately?

If we can consider them as one trade this would be an opportunity to still take advantage of losses, as follows:

Example: Selling crypto acquired over multiple Transactions

Say we’ve made the following trades

| Date | Type | Amount | Price |

|---|---|---|---|

| January 15th | Purchase | 1 ETH | 1000 EUR |

| February 15th | Purchase | 1 BTC | 3000 EUR |

The current market price for each ETH is 2000 EUR. Therefore, we know that if we sell the first ETH, it would result in a 1000 EUR gain, and if we then sell the second ETH it would result in a 1000 EUR loss we could not deduct.

But what if we can sell both Ethereum at once?

Wouldn’t we then be selling 2 ETH for 4000 EUR, which has been acquired for 4000 EUR? We would incur no loss?!

Sadly we cannot do what we’ve just done in the example. The EMTA has clarified that we have to calculate the gain/loss by acquisition. So if we are selling 2 ETH acquired over 2 transactions, we’ll have to calculate the gain or loss for each acquisition. First we’d incur a 1000 EUR profit on the first ETH sold, then a 1000 EUR loss on the second ETH sold. The 1000 EUR loss will then be irrelevant for our taxes

Tax Treatment of Different Cryptocurrency Transaction Types

There are differences between transactions in how they contribute to your taxes and how they are declared. So, we will break down all of the transaction types here.

If you’re doing your taxes with Divly, Divly's report will show you what you have to declare and where

We'll cover all of the following transactions:

-

Buy Crypto

-

Sell Crypto

-

Trade Crypto for Crypto

-

Purchase Goods & Services

-

Paying Trading/Transfer fees with Crypto

-

Transferring Crypto between your own wallets

-

Lost/Stolen Crypto

-

Giving/Receiving Cryptocurrency as a gift

-

Donating Crypto

-

Airdrops

-

Forks

-

Mining

-

Income

-

Interest

-

Staking rewards

-

Futures/Derivatives

-

NFTs

Buy Crypto with Fiat (EUR, USD, etc)

When buying cryptocurrency for a fiat currency, you won’t be taxed. However, it is important to keep records of your purchase costs, including fees, so that you can deduct these from your future sales.

Selling Crypto for Fiat (EUR, USD, etc)

How is it taxed?

If you sell cryptocurrency, you will have to pay income taxes on the difference between the sale price and the purchase price. If you incur a fee to facilitate the trade, you can deduct this cost from your sales price. However, any losses incurred cannot be deducted from the gains.

Where is it declared?

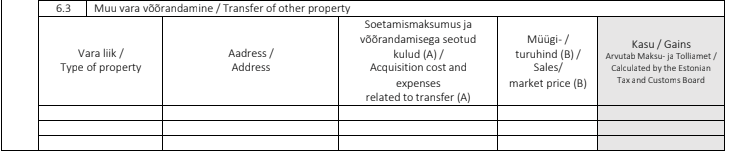

Income received through selling crypto must be declared in tables 6.3 or 8.3 of the income tax return.

Gains made on foreign exchanges must be reported in table 8.3, and gains made on local exchanges must be declared in table 6.3. Divly will split your gains by exchange so that you can easily determine whether the gain belongs in 6.3 or 8.3

You should declare all of your profitable transactions in these tables. If you have a large number of transactions you may either use an additional appendix sheet, or you may choose to consolidate your transactions by exchange/platform used, as long as you can provide an itemized list of your transactions. Divly will group transactions for you automatically as well as provide you with an itemized list you can submit.

For cryptocurrency transactions, you can enter Cryptocurrency under the Type of property field. You can leave the field Address empty.

Trading Cryptocurrency

How is it taxed?

When you trade one cryptocurrency for another, you can still incur a taxable profit. This will be the case if the selling price of the trade is larger than the purchase price of the currency you are trading away.

Example: Crypto-to-Crypto Trade

Say you make the following transactions

| Date | Type | Amount | Price |

|---|---|---|---|

| March 10th | Purchase | 1 SOL | 50 EUR |

| March 12th | Trade | 1 LTC | 1 SOL (Valued at 70 EUR) |

In this case you will have incurred a taxable profit of 20 EUR when you've traded your SOL for LTC.

Warning! Do be careful with trading cryptocurrency. When you invest in regular stocks and sell them, you can put aside some of the money you earn to pay your taxes later. When you trade crypto, you are still invested in crypto. There is no money put aside to pay your taxes. If you’ve made a profit and after December 31st, all of your crypto drops to 0 euros, you would still have to pay taxes on the profits. So make sure you also sell enough to cover any tax expenses.

Where is it declared?

Income received through selling crypto must be declared in tables 6.3 or 8.3 of the income tax return.

Gains made on foreign exchanges must be reported in table 8.3, and gains made on local exchanges must be declared in table 6.3. Divly will split your gains by exchange so that you can easily determine whether the gain belongs in 6.3 or 8.3

Purchase Goods & Services with crypto

How is it taxed?

When you purchase a good or service with crypto you may incur a taxable gain. The gain is equal to the value of the good or service purchased minus the initial acquisition cost

Where is it declared?

Income received through selling crypto must be declared in tables 6.3 or 8.3 of the income tax return.

Gains made on foreign exchanges must be reported in table 8.3, and gains made on local exchanges must be declared in table 6.3. Divly will split your gains by exchange so that you can easily determine whether the gain belongs in 6.3 or 8.3

Pay Fees with cryptocurrency

How is it taxed?

You can add purchase expenses to your cryptocurrency purchase costs, and deduct selling expenses from the sale price thereby lowering your taxes.

However, if the fee is paid for in crypto then this is seen as a sale of your cryptocurrency. In this case you will have to pay taxes if you incur a gain.

Where is it declared?

Income received through selling crypto must be declared in tables 6.3 or 8.3 of the income tax return.

Gains made on foreign exchanges must be reported in table 8.3, and gains made on local exchanges must be declared in table 6.3. Divly will split your gains by exchange so that you can easily determine whether the gain belongs in 6.3 or 8.3

Transferring Crypto between your own wallets

Transferring crypto between your own wallets and exchanges is not a taxable event. However, if you incur any fees paid with crypto to facilitate the transaction you may have to pay taxes on the increase in value of this crypto since it’s acquisition.

Lost/Stolen

When you lose possession of your cryptocurrency this is usually taxed. In the case where your cryptocurrency is stolen or lost this is not the case. Whether you can deduct the cost of your lost/stolen crypto is a matter you should bring up with a tax professional so that you can discuss your specific circumstances.

Giving/Receiving Cryptocurrency as a gift

How is it taxed?

Receiving cryptocurrency as a gift is not a taxable event. However, if you receive a cryptocurrency gift and convert it to a fiat currency such as euros, then you will incur taxes on the sales price.

You cannot inherit the acquisition cost from the person who gave you the gift. The acquisition cost is set to 0 euros, and you are therefore taxed on the full amount once you sell or trade the cryptocurrency received through the gift.

Where is it declared?

In the case that you sell your cryptocurrency gift for fiat, or another cryptocurrency, then you can enter the profits in tables 6.3 or 8.3 depending on whether you’ve conducted the transaction on a local or foreign platform.

Donating Cryptocurrency

How is this taxed?

If you’ve made any gifts or donations to a non-profit organization,foundation or religious association with income tax benefits specified in § 11 subsection 1 of the Income Tax Act or specified in § 11 subsection 10 then you will not incur any taxes on the disposal of your cryptocurrency

Furthermore you can deduct your donations from your income up to 1200 euros!

Where is this declared?

If you’ve made any gifts or donations to a non-profit organization,

foundation or religious association you can declare this in table 9.4 of your income tax return

Airdrops

How is it taxed?

You are not taxed when you receive cryptocurrency through an airdrop. Only once you sell the cryptocurrency received will you have to pay taxes over the sales price of the cryptocurrency

Forks

How is it taxed?

You are not taxed when you receive cryptocurrency through a fork. Only once you sell the cryptocurrency received will you have to pay taxes over the sales price of the cryptocurrency

Mining

How is it taxed?

The mining of cryptocurrency is considered a business activity. If you are a private person, you have to declare your mining income as business income from a natural person. You cannot deduct any mining expenses such as equipment and electricity. If you permanently mine cryptocurrency and register as a sole proprietor, then you can deduct equipment expenses.

You are taxed on the value of the mined coins at the time you trade or sell them.

Where is it declared?

You should declare your mining income in Form E, on line 1.1.10.

Receive Income in crypto

How is it taxed?

If you receive remuneration or wages in cryptocurrency on which income tax has not been withheld, then you must declare the value of the cryptocurrency in terms of euros to the tax authorities.

Where is it declared?

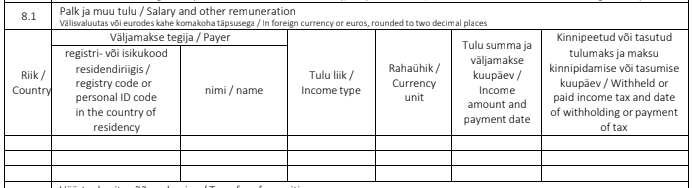

You should declare income from an Estonian employer in part 2 of table 5.1 of your tax return, and income from a foreign employer in part 2 of table 8.1 of your tax return.

Interest & Loans

How is it taxed?

Lending your cryptocurrency to a company and receiving the same cryptocurrency amount in return is not a taxable event, even if its value has risen since you first acquired it.

However, if you lend cryptocurrency and are repaid in a different currency, such as euros, taxes must be paid on any appreciation in value from the time you originally acquired the cryptocurrency.

Furthermore, if you earn additional cryptocurrency as interest for lending out your crypto assets, this must be reported as income. The value of the interest earned should be calculated based on the cryptocurrency's market value at the time it was received.

Where is it declared?

If you are paid back on your loan in a fiat currency you will have to declare your gain/loss in tables 6.3 / 8.3 of the income tax return.

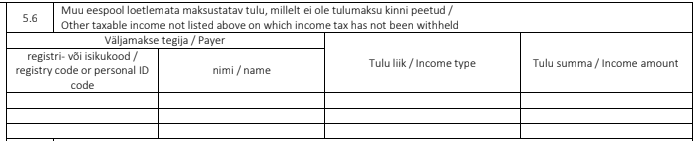

You should declare your interest income in table 5.6 of your income tax return

Staking rewards

How is it taxed?

If you receive staking rewards you will be taxed on the value of the cryptocurrency received at the time you received it.

Where is it declared?

You should declare your staking income in part 2 of tables 5.1 for income earned on Estonian platforms, and part 2 of table 8.1 for foreign platforms.

Staking rewards can easily result in many different transactions. Luckily you can consolidate your staking rewards as long as they occurred on the same platform and you provide an itemized list of all of your staking rewards. Divly will automatically consolidate your staking rewards by exchange and provide you with an itemized list of your transactions.

However, there are only three rows to fill in your income tax return. If you’ve used four exchanges you and are filing your tax return on paper do make sure to use an additional appendix sheet that corresponds with table 5.1 or 8.1.

For table 8.1 you will additionally have to enter a date for the staking rewards. As you are likely consolidating your staking rewards you should enter 31.12.202(3) depending on the year in which the transaction occurred.

Futures/Derivatives

How is it taxed?

You will have to pay taxes on any realized gains from your transactions. You cannot deduct any realized losses from your gains

How is it declared?

Gains made on foreign exchanges must be reported in table 8.3, and gains made on local exchanges must be declared in table 6.3. Divly will split your gains by exchange so that you can easily determine whether the gain belongs in 6.3 or 8.3

Trading NFTs

How is it taxed?

If you use cryptocurrency to purchase an NFT, or sell an NFT for a cryptocurrency or fiat, then these are taxable transactions. You will be taxed on the increase in value of the sold cryptocurrency/NFT at the time of the transaction

Where is it declared?

Income received must be declared in tables 6.3 or 8.3 of the income tax return.

Gains made on foreign exchanges must be reported in table 8.3, and gains made on local exchanges must be declared in table 6.3. Divly will split your gains by exchange so that you can easily determine whether the gain belongs in 6.3 or 8.3

How can I calculate my cryptocurrency taxes?

The easiest way to complete your cryptocurrency tax declaration is by using tax software. The EMTA specifies that you can choose the most suitable software for you as long as the calculation process is traceable and complies with Estonian taxation rules.

Therefore, it is important to choose crypto tax software that follows Estonian regulations. As of January 2026, Divly is the only software built to help Estonian tax payers on their crypto taxes, following Estonian regulations.

Some of the benefits of Divly are:

-

Supports over 150+ cryptocurrency exchanges, with an easy import of your transaction history.

-

Automatically classifies your transactions and treats them accordingly, following Estonian regulations.

-

Performs all of the required tax calculations for you.

-

Provides you with a document that guides you through your declaration and lets you know what needs to be declared where.

-

Provides you with a transaction history file that follows the specifications required by the EMTA.

How do I declare my cryptocurrency taxes?

Once your tax calculations are complete and EMTA’s tax portal opens in February, you can begin your declaration.

For your tax declaration you’ll have to know about two forms, Form A which is your Income Tax Return Of A Resident Natural Person, and if you’ve mined cryptocurrency you’ll also have to fill in Form E, for Business Income Of A Resident Tax Person.

Form A

Salary and Other remuneration on which income tax has not been withheld (Table 5.1 / 8.1)

If you’ve received income/or wages in cryptocurrency for which taxes have not been withheld you should declare them in table 5.1 part 2. If the employer is located in Estonia, and in table 8.1 part 2 if they are located abroad.

You should also declare your income from staking rewards in this section. Luckily, you are allowed to group your staking reward income by exchange. In this way you avoid having to declare every transaction individually. If you consolidate your information you must provide an attachment of your transaction history and the corresponding pricing information.

For table 8.1 you will also have to fill in the payment date. If you have consolidated your income you can enter 31.12.202(3) depending on the year in which the transactions occurred.

Other taxable income not listed above on which income tax has not been withheld (Table 5.6)

If you receive any interest as a result of lending your cryptocurrency, you should include this in table 5.6 of your income tax return.

Transfer of other property (Table 6.3 / 8.3)

Most of your transactions will be declared here. Income on Estonian platforms must be declared in table 6.3 and income from abroad must be declared in table 8.3.

Here too you can group transactions together by exchange, as long as you can provide an itemized list of all of the calculations performed.

You can leave the address column empty for cryptocurrency declarations. The other fields can be provided to you by Divly.

Form E

Form E can be used to declare your mining income as a natural person. Do be aware that you cannot include any expenses for your income

You can declare your mining income in line 1.1.10 for "other income".

FAQ

Will the Tax Authority Know About My Crypto Transactions in Estonia?

Due to the new EU directive DAC8, it is highly likely that the Estonian Tax and Customs Board will become aware of your crypto transactions. According to this directive, which comes into effect on January 1, 2026, all cryptocurrency platforms are required to share data on the trading activities of EU citizens with the tax authorities.

Therefore, the Estonian Tax and Customs Board will gain insight into your crypto trading activities.

Is it possible to correct an already submitted income tax return if crypto transactions were not declared?

Yes, it is. The tax return can be retroactively submitted and corrected within three years. If you wish to correct a submitted income tax return, please contact the Tax and Customs Board's customer support by e-mail [email protected]

Are there ways to lower my cryptocurrency taxes?

If you’ve already sold your cryptocurrency then there is no way to lower your taxes for those transactions. Once sold, if you realize a profit, it will be taxable.

However, there are a few ways to lower your crypto taxes. If you are making a crypto to crypto trade, you can use a crypto tax tool such as Divly to test transactions you plan on making. In this way you can determine which cryptocurrency would be most beneficial to sell to lower your taxable profit.

Unfortunately you cannot use an investment account for cryptocurrency as cryptocurrency is not defined as a financial asset as per subsection 17(2) of the Income Tax Act. Therefore, the option to postpone your tax liability is not available to you.

Therefore the best ways to lower your taxes are not to sell your investment, or if you must sell/trade, to take into account the profit or loss that would occur for each coin you could sell.

Any tax-related information provided by us is not tax advice, financial advice, accounting advice or legal advice and cannot be used by you or any other party for the purpose of avoiding tax penalties. You should seek the advice of a tax professional regarding your particular circumstances. We make no claims, promises, or warranties about the accuracy of the information provided herein. Everything included herein is our opinion and not a statement of fact.