Do you need some help with cryptocurrency taxes or have questions about crypto taxes in New Zealand? Don’t worry. Crypto taxation is a very new topic. We made this guide to tell you everything you’ll need to know for your tax declaration to the Internal Revenue Department.

If you’re on a desktop and want to skip to a section quickly, you can use the table of contents to the side of this guide. If you’re on mobile, you can burn 20 calories per hour by scrolling.

This guide will be updated and maintained regularly to account for changes made by the local tax authority (Inland Revenue) and new types of transactions. Suppose you find any errors or outdated information. In that case, it is greatly appreciated that you let us know by sending an email to [email protected] or via our support chat at the bottom right corner of our website.

Important dates 2022

The tax year in New Zealand runs from 1 April to 31 March. All crypto transactions between those dates must be considered for your tax return.

July 7th – Deadline to declare your taxes

March 31st – Extension deadline if you have a tax agent

How are cryptocurrencies taxed in New Zealand

In New Zealand, you are taxed on your income from mining, staking, selling, or trading cryptocurrency. You will have to pay taxes based on your income tax bracket of 10.5% to 39%. However, you can offset your cryptocurrency losses from your other income sources.

Your cryptocurrency income likely comes from any of the following activities

-

Mining

-

Staking

-

Lending

-

Selling

-

Trading

-

Getting paid for goods & services

-

NFT transactions

-

In some cases, airdrops and forks

You are taxed on your cryptocurrency transactions if your primary purpose of acquiring crypto was that of disposal. Likewise, you can use your crypto losses to offset other income only if the primary purpose of acquiring crypto is disposal.

What is my Purpose?

The primary determinant of whether you are taxed on cryptocurrencies is the purpose for which you acquired the cryptocurrency. If you hold cryptocurrency for the purpose of disposal (e.g, selling) then your disposal transactions are taxed.

Although you may have more than one purpose, it is your primary purpose for acquiring cryptocurrencies that you had at the time that matters for your taxes.

Any of the following may help you determine your purpose for acquiring cryptocurrency

-

Nature of the asset (What are the benefits besides potential increases in value from owning this cryptocurrency

-

Circumstances of the purchase

-

Number of similar transactions

-

How long do you plan to hold the asset

Although the following scenarios may initially seem as if the primary purpose is not disposal, upon closer inspection, they are still acquired for disposal.

· Long-term investment

· Hedge against inflation

· Portfolio diversification

· Store of value

Don’t worry. We will provide multiple examples throughout the guide on when you can be expected to pay taxes and when not.

In most cases, your cryptocurrency was acquired for disposal and will therefore be taxed.

If you are uncertain, we recommend contacting a tax lawyer or the IRD to ask for clarification on your situation. Otherwise, it is safest to assume that you acquired your cryptocurrency for the purpose of disposal.

Can I offset losses made on crypto from other income?

The crypto crash has not been kind to most crypto investors. The total crypto market cap crashed from $4.7trillion to $1.4 trillion between November 2021 and July 2022.

Luckily, in New Zealand, you can use your losses to offset income made elsewhere, lowering your tax bill.

It is essential to know that you can only declare a loss if you’ve made a loss on the disposal of your cryptocurrency. If your cryptocurrency has only decreased in value and you’ve not sold it, it does not count as a loss.

If you plan to indicate that you’ve made a loss, then you must be able to prove that if you had made a gain, you would be taxed. Again, what matters here is your purpose. If you bought cryptocurrency for disposal, then it is taxable at the time of disposal.

You should declare your cryptocurrency net income under Q28 on the IR3. So if you’ve made losses, you can also enter them here.

What is the tax rate for cryptocurrencies?

In New Zealand, you will primarily be paying income tax on your crypto income. Therefore, crypto is taxed at your regular income tax rate.

| Taxable Income (NZD) | Tax Rate % |

|---|---|

| 0 – 14,000 | 10.5 |

| 14,001 – 48,000 | 17.5 |

| 48,001 – 70,000 | 30 |

| 70,001 – 180,000 | 33 |

| 180,001+ | 39 |

Source: IRD

Example: Jonas has an income of 75,000 NZD, which includes his crypto income. Then his income tax will be (14,0000.105)+(340000.175)+(22000.30)+(5000*.33) = 15,670 NZD.

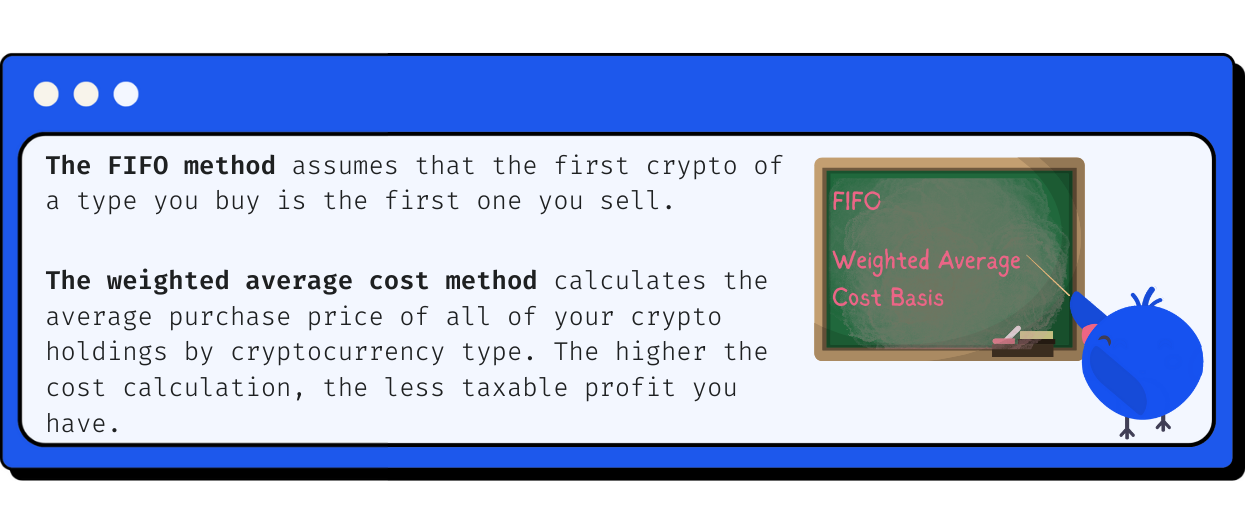

Cost Basis Calculations

Suppose you are doing your crypto calculations manually. Then you may want to read this section. If you’re using a cryptocurrency tax calculator like Divly, feel free to skip this.

Which cost should you allocate to your crypto? The acquisition costs of the cryptocurrencies are determined by their market value at the time of acquisition. Once you sell a cryptocurrency, you can subtract the acquisition cost from the sale price to determine your profits.

If you cannot separately identify which crypto asset is part of which sale, you can use either the FIFO (first-in first-out) or the Average Cost Basis method.

You must use the same method from year to year.

Example: On 4 May 2016, Michael purchased 1 BTC for 500 NZD. On 15 January 2022, he purchased 1 BTC for 50,000 NZD. Then on 16 January 2022, he sold one 1 BTC for 40,000NZD.

Using the FIFO method, we assume the first purchased BTC is the first one sold. So his sale transaction leads to an income of 40,000 NZD – 500 NZD = 39,500 NZD.

Using the Weighted Average method, the cost associated with the sale will be (50,000+500)/2 = 25250. So Michael will have made a profit of 40,000 NZD - 25250 NZD = 14750 NZD

Tax Residence and Taxes

If you are a New Zealand tax resident you should pay tax on worldwide income. Therefore, you will also pay tax on crypto income, even if you’ve used wallets or exchanges outside of New Zealand, or conducted transactions overseas.

If you are a new tax resident, you may be considered a transitional tax resident, and certain benefits will apply. You’ll be able to benefit from a four-year tax exemption on foreign income. This includes crypto income (whether you acquired them before becoming a New Zealand tax resident or after).

However, keep in mind that selling cryptocurrency on a New Zealand-based exchange is not exempt from these taxes.

Am I taxed as a business or an individual?

Most people will simply be taxed as an individual. But if you are unsure, you can read this next section to understand better whether you would be taxed as a business or as an individual.

If you work full-time and trade crypto on the side, you will likely not be considered taxable as a business. However, you will still need to pay taxes on any gains you’ve incurred. You’ll likely be considered in the business of trading cryptocurrency if you

· Have a high number of transactions

· Spend significant time managing your crypto activities

· The managing of your crypto portfolio is done on a regular basis.

You can find a number of examples of when you would be considered a business on the IRD website.

You may also be taxed as a business if you mine cryptocurrency. The factors to consider are

-

How long have you been mining, or intend to mine

-

The size of your mining operation

-

How much time and money you use to mine

-

Do you have a profit motive

The longer you mine, the larger your mining operation, and the more time and money you invest, the likelier your activity is seen as a mining business. You can see some examples laid out by the IRD on whether you would be considered a business here.

GST Tax

GST tax is 15%. Generally, cryptocurrency trading and selling are not subject to GST tax. However, in some cases, you may be subject to GST tax. This includes mining, NFT transactions, or providing goods & services.

If you believe you’ll earn more than $60,000 in a 12-month period on GST taxable transactions, then you must register for GST.

NZ Crypto tax treatment of different transaction types

Different types of transactions will behave differently for tax purposes. You can use this table to get a quick overview of how certain transactions are taxed.

We also have more detailed information about each transaction type below the table

| Transaction Type | Tax Classification | Divly Classification |

|---|---|---|

| Buy Crypto | None | Buy |

| Sell Crypto | Income Tax | Sell |

| Trade Crypto For Crypto | Income Tax | Traded crypto |

| Initial Coin Offering (ICO) | Income Tax | Traded Crypto |

| Purchase Goods & Services | Income Tax* | Goods/Services |

| Pay Trading Fee with Crypto | Income Tax | Fee Included in Trade |

| Pay Transfer Fee with Crypto | Income Tax | Fee Included in Transfer |

| Transfer Crypto Between Your Wallets | None | Transfer |

| Lost or Stolen Crypto | None (deductible) | Lost/Stolen |

| Give Crypto as a Gift | None* | Gifted Away |

| Receive Crypto as a Gift | Income Tax* | Received Gift |

| Donate Crypto | None | Donation |

| Airdrop | None* | Airdrop |

| Hard Fork | None* | Fork |

| Mining | Income Tax / GST Tax | Mining |

| Staking | Income Tax / GST Tax | Staking Reward |

| Income (e.g., freelancing, salary) | Income Tax | Income |

| Lend out crypto | Income Tax | Interest Received |

| Borrowing crypto | Income Tax | Interest Paid |

| Margin Trading | Income Tax | Realized Profit/Loss |

| NFTs | Income Tax/ GST | Trade, Sell |

Buy Crypto / Buy Crypto with Fiat

There are no taxes involved when buying crypto. However, you need to ensure that you keep track of the price you paid for it for your cost basis calculation.Cryptocurrency/digital token valuations for cost and revenue calculations are based on the value at the acquisition time.

If you purchased the crypto in a foreign currency (e.g., USD or SEK), convert it to the value in local currency on that day.

The IRD asks you to be reasonable and careful when determining the NZD value of your crypto assets. Generally, you may use an authoritative cryptocurrency tracking website such as Coinmarketcap or Coingecko.

Sell Crypto / Sell Crypto for Fiat

If you’ve made a gain on the sale of a cryptocurrency, you will have to record the profits for personal income tax purposes. If you incurred a loss, you can offset it from income if you’ve acquired the crypto for the purpose of disposal.

Trade Crypto for Crypto

As with selling cryptocurrency for fiat, you will be taxed on crypto to crypto transactions. Any gain incurred must be declared for income tax purposes.

Initial Coin Offering

An ICO is a way for blockchain companies to sell pre-mined crypto to potential investors. When you invest your crypto (usually Ethereum) in a new project, you are provided a token for that project.

The IRD has not provided explicit guidance for those who partake in ICOs. But from a taxation point of view, this likely works the same as a crypto-to-crypto trade. Essentially, you send cryptocurrency in exchange for a token from a new project. You follow the same principle where you sell your crypto for the value of the ICO token in local currency. The crypto you send is subject to personal income tax, and the received token inherits its cost basis.

Purchase Goods & Services with Crypto

Spending crypto to purchase goods & services is a crypto disposal event. Therefore, you will be subject to taxation on any gains incurred. If you are receiving crypto as compensation for providing goods & services, you also have to charge GST taxes.

Pay Trading/Transfer Fees in Crypto

On some exchanges, typically, when you trade crypto for crypto, you will pay the trading fee in crypto. In these cases, you need to convert the crypto you used to pay for the trading fee into your local currency and then pay capital gains. This can become quite tedious if you have many trades.

You can deduct the cost of your crypto assets when calculating income. This includes any transaction fees incurred.

Transfer Crypto Between Your Own Wallets

Transferring crypto between your wallets is not a taxable event (this includes sending crypto to your account on an exchange). Only the transfer fee is taxed as described in the section above. You must track these transfers properly, so you don’t pay unnecessary taxes!

A cryptocurrency calculator like Divly will be able to automatically determine which transactions were transfers.

Lost or Stolen Crypto

You do not need to pay taxes on lost or stolen crypto. In some situations, you can claim a loss equal to the initial value of the stolen crypto assets. The amount you can claim is the amount you paid to acquire them. So unlike with other disposals, the fair market value at the time is irrelevant.

You can only claim the loss if the crypto was taxable if you would have sold or traded it. You need to be able to show the following

-

Your crypto asset was stolen

-

If your crypto asset had not been stolen, then any income earned on its disposal would have been taxable.

-

You have not been able to recover your crypto.

If you manage to retrieve your stolen income and you have previously received a deduction for this asset, then you will have to declare the value of the recovered crypto as income. This amount is generally limited to the amount that has been declared as a loss.

Give Crypto as a Gift / Receive Crypto as a Gift

If you’ve made a gift after 1 October 2011, you will not pay a gift tax. However, you may still want to check whether you’ve met the legal requirements for a gift.

Donate Crypto

There are no concrete guidelines for cryptocurrency donations. However, generally, you can claim 1/3rd of any amount above $5 donated to approved charities and organizations. To be eligible for a deduction you must have made taxable income in the year in which you’re claiming a donation.

Example:

You have a taxable income of $10,000 and donate $6000 worth of BTC to an approved charity. You can then get donation credits totaling $2000.

Airdrop

An airdrop is typically considered a gift from the token holder or blockchain. You may be taxed upon receipt, disposal, or both for airdrops.

If you passively acquire crypto through airdrops, then generally you won’t be taxed upon the receipt of the airdrop.

Receipt of airdropped coins is taxable if you

-

Receive airdrops regularly

-

Have performed services to receive the airdrop

-

Have a cryptoasset business

-

Acquire the cryptoassets as part of a profit-making scheme.

Small actions such as filling in Know-Your-Customer information to receive an airdrop are insufficient to be seen as performing a service that results in taxable income.

Disposal of airdropped coins is taxable if you

-

Dispose of crypto assets as part of a profit-making scheme

-

Provided services for the airdrop

-

Have a crypto asset business.

-

Acquired the crypto assets to dispose of them

Providing a service to receive an airdrop may be as simple as performing an action such as liking a post or sharing a tweet. If you performed such an action, then you’ve had a purpose for acquiring airdropped cryptocurrencies. If this purpose is to dispose of the airdrops and make a profit, then the disposal is taxable.

If you are taxed at both the receipt and disposal of the airdropped crypto asset then you can deduct the value declared upon receipt from the disposal value when calculating income. In this way, you will not be taxed twice on the same amount.

Example:

Maria knew that holders of cryptocurrency ABC would receive an airdrop of cryptocurrency XYZ. She thought receiving XYZ could be profitable. She purchased some ABC and filled in general Know-Your-Customer information to sign up for the airdrop.

Maria received $5 worth of ABC from the airdrop. The receipt of the airdrop is not taxable. However, as the acquisition of the airdrop was done with the purpose of disposal, any transactions she makes with ABC will be taxable.

Hard Fork

A hard fork occurs when a blockchain splits. You may receive a new currency if you hold the original cryptocurrency. For hard forks, you may be taxed upon the receipt, disposal, or both. Generally, if you passively acquire crypto through a fork, it will not be taxed. The receipt of a fork will only be taxable if you

-

Have a crypto asset business

-

Acquired the crypto assets as part of a profit-making scheme.

Disposing of your crypto received from a fork will be taxable if you

-

Have a crypto asset business

-

Disposed of the crypto assets as part of a profit-making scheme

-

Acquired the crypto assets with the purpose of disposing of them

-

Acquired the original crypto assets for the purpose of disposal.

The received cryptocurrency inherits the purpose for which you acquired the original crypto asset. If your primary purpose for acquiring the original crypto asset was for disposal, then you will have also acquired the forked currency for disposal. If the forked crypto asset has been acquired for disposal, then it will be taxed on any trades you make using it.

General tax treatment if acquiring a forked crypto asset:

General tax treatment for selling a forked crypto asset:

Example:

Maria purchased Bitcoin because she believed it would increase in value, and she wanted to profit off of this value increase. She traded some Bitcoin along with other cryptocurrencies here and there.

On 1 August 2017, Bitcoin forked, and Maria received some Bitcoin Cash on the exchange she was using. Maria has since traded with her Bitcoin Cash. Maria will not be taxed on the receipt of the Bitcoin Cash. She will have to pay taxes on all Bitcoin Cash transactions she makes as the currency was acquired for the same reason as her Bitcoin for disposal.

Mining & Staking

Generally, any block rewards or transaction fees you receive from mining or staking crypto will be taxable. If you mine cryptocurrencies, you will have to pay taxes if you

-

Earn ordinary income from providing mining services.

-

Mine crypto assets for disposal

-

Are in the business of mining crypto assets

-

Participate in a profit-making scheme.

In most cases, you will be taxed at the receipt and disposal of your mined/staked cryptocurrency. Again your purpose for which you are staking matters. For example, suppose you stake a cryptocurrency with the belief that the currency would increase in value in addition to receiving staking rewards. In that case, you’re likely staking for disposal. In this case, selling staking rewards is taxable. If you sell your cryptocurrency and claim it was not acquired for disposal you need to be able to prove it.

You can deduct depreciation expenses for any computer hardware or software used for mining/staking.

If you are in the business of mining cryptocurrency you may have to pay GST tax when you earn cryptocurrency from mining

In most cases, for GST purposes, your mining rewards will be zero-rated. This is the case if the blockchain you are mining is ‘situated’ outside of New Zealand. Therefore, you do not need to pay GST tax on your received cryptocurrency. However, once you sell, you will have to pay income tax on any increase in value that occurred since the cryptocurrency was mined.

Lending Crypto and Loan Interest

Any crypto earned from lending will also be part of your crypto asset income. You must report the fair market value at the time of receipt of any cryptocurrency interest you receive.

Income and Rewards

Although no concrete guidelines have been provided on crypto income, you generally have to pay income tax if you’ve performed any work or effort in acquiring crypto. This includes simple actions like sharing a tweet or learn-to-earn programs like Coinbase Earn.

Margin Trading & Futures

Margin trading involves borrowing to take leveraged positions on crypto. The IRD does not explicitly mention margin trading in its guidance for cryptocurrencies.

Because of the complexity of the subject, you may have questions about the tax treatment of your crypto assets, and it may be worthwhile to contact the IRD and ask them directly about your specific situation.

Generally the outcome of the trades is provided as realized profit or loss after margin fees are accounted for. In these cases, the realized profit or loss is taxable.

Tax treatment of NFT

NFTS(Non-fungible tokens) can be a hobby, profit-making scheme, or business. If you transact in NFTs for the enjoyment of the art, no tax is due on disposal.

However, if your primary purpose for buying and selling NFTs is to hold them as an investment or to dispose of them, then you have to pay taxes on your NFT income. Keep your frequency of transactions and your intended time to keep an NFT in mind when determining your primary purpose with NFTs.

NFTs, unlike cryptocurrency trading, are subject to GST. Therefore if you’ve made more than $60,000 from NFTs, you must register for GST. If you sell NFTS to New Zealand residents, then you must pay GST. The transaction will be zero-rated for GST purposes if sold outside of New Zealand.

Example:

Michael has an interest in NFTs. He’s been creating NFT artwork for some time but has full-time employment elsewhere. Michael has earned $65,000 on his NFT work in one year.

Michael may not have a business, but he has a profit-making scheme. Michael has to declare this NFT income and pay GST tax if any sales are known to be to New Zealand residents.

How to calculate your cryptocurrency Income

New Zealand’s Internal Revenue Department recognizes the complexities of declaring your cryptocurrency taxes. Therefore they recommend that you use a cryptocurrency tax calculation tool such as Divly to automate your taxes.

Divly is a cryptocurrency tax calculator built around IRD’s guidance. Simply sync your trading history from your wallets & exchanges with Divly, and Divly will do the calculations for you.

It is free to get started with Divly

You can import up to 20,000 transactions for free to get an overview of all your cryptocurrency activity. Track your holdings and see your profits or losses on each transaction.

Track your portfolio

Divly has extensive tracking features for your cryptocurrency portfolio.

-

ROI Tracking Follow your cryptocurrency portfolio’s value over time and compare this with your investment costs.

-

Currency Overview. What percentage of your portfolio consists of a specific coin? What’s its value, and where is it held?

-

Income Summary. Determine the source of your crypto income. Whether mining, staking, interest, margin trading, gifts, or more.

-

Heaps of supported integrations. Divly supports over 60 wallets & exchanges and over 7000 currencies.

Are we still missing an altcoin or an exchange you are using? Reach out to our dedicated support team!

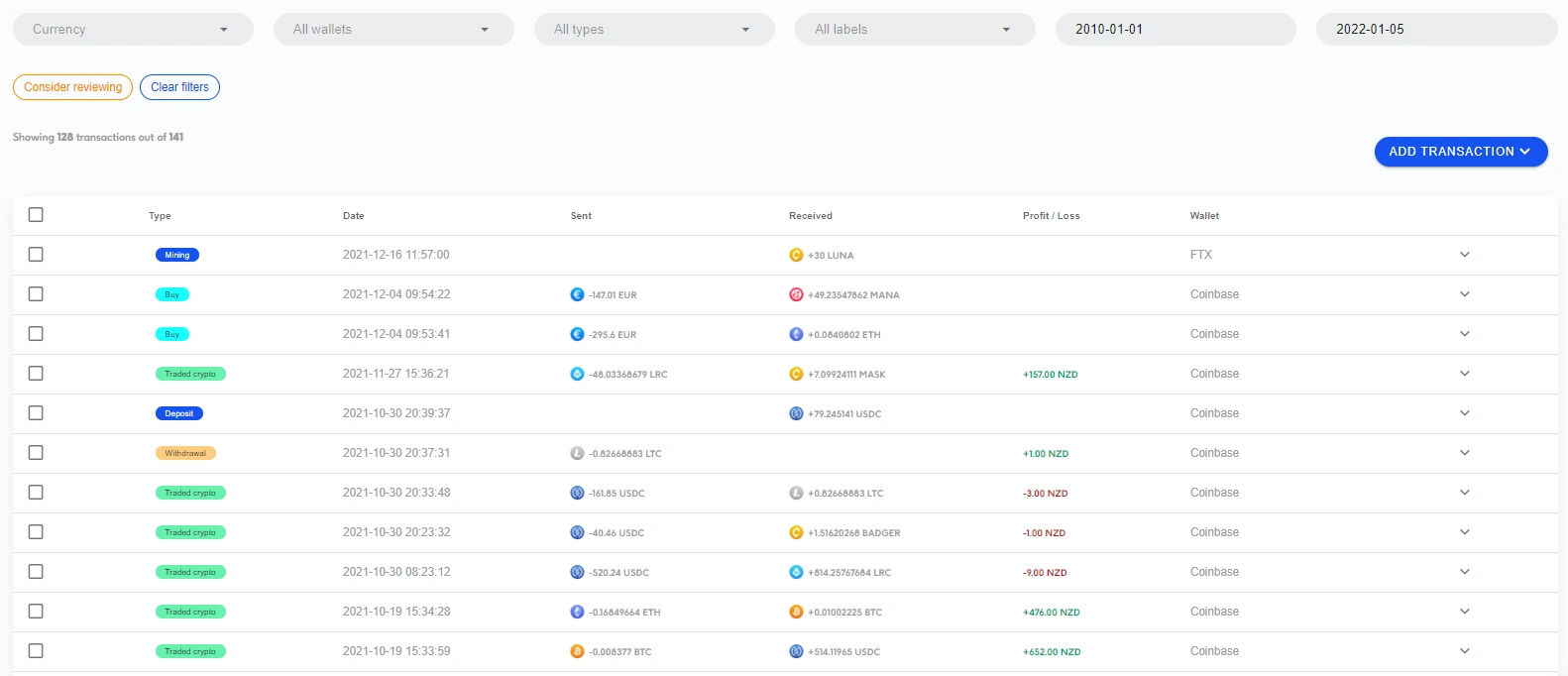

One page. All of your transactions.

No need to shuffle through tens of pages to see all of your transactions. All your transactions are in one place.

-

Multiple Data Import Methods. Connect via API, CSV, custom data entry, or just copy-paste in your blockchain wallet address. We’ll import and analyze the transactions for you.

-

Smart Transfer Matching. Made too many transfers between your exchanges? Have difficulty keeping track? Divly will automatically detect and match transfers for you.

-

Batch Editing. Divly provides a simple method to batch edit many transactions at once. This can save considerable time for your taxes.

-

Automatically labels your transactions. Divly automatically distinguishes between cryptocurrency activities such as mining, staking, interest, airdrops, forks, and many more. This way, you get a better overview of your activity, and each activity can be taxed accordingly.

-

Warnings. Does it seem like you’ve not uploaded all of your transactions? Divly will look for potential issues in your transactions to point them out and avoid any problems.

Divly is built around the Internal Revenue department’s Guidance

-

Tailored Tax Report. Divly’s tax report contains everything you need to declare to Inland Revenue. In addition to calculating your overall net income, Divly’s tax export also provides your income by exchange or wallet should you be a new tax resident and only have to pay tax on cryptocurrency income earned in New Zealand.

-

Build With Purpose in Mind. Generally, most cryptocurrency transactions are taxed in a specific way and have a precise treatment by Divly. However, the purpose with which you acquire cryptocurrencies matters in New Zealand! Other cryptocurrency tax calculators only allow you to use one tax rule for each transaction type. Divly is the only cryptocurrency tax calculator that respects the nuance of your situation and distinguishes between the tax treatment within labels.

Many more features

See our product page for more information on how Divly is tailored for New Zealand.

How to submit your tax report to Inland Revenue

Once all the tax calculations are done, and Inland Revenue’s tax portal is open, it’s time to declare your taxes before the deadline in July. You should file an individual income tax return if you’ve made cryptocurrency income. You can report your taxes both via mail using a paper filing or online using myIR. If you would like to do a paper filing, you can download the latest IR3 here.

If your crypto income does not fit into other boxes, such as self-employed income or business income, then it should be declared as other income. Other income can be found under question 28 on the IR3.

Your Divly tax export will include all the information needed to declare your taxes to the IRD.

You must keep a record of your cryptocurrency transactions that include the following:

· The type of crypto asset

· Date of the transaction

· Type of transaction

· Number of units

· Value of the transaction in NZD

· Total units of each crypto asset held at the beginning and end of the year

· Exchange records and bank statements

· Wallet addresses

You need to keep these records for at least seven years. Using crypto asset exchanges, you should download your transaction history regularly. Crypto asset exchanges may only keep records for a short time, or the exchange may no longer exist when you do your tax return.

Paying GST

If you conduct a taxable activity with a turnover of at least $60,000 in a 12-month period or you add GST prices to any services you deliver, then you have to register for GST. Once registered, you need to start filing GST returns. You can choose to file your GST returns monthly, every two months, or half yearly, with some restrictions based on the sales volume.

You need to calculate the difference between your paid and received GST. If you’ve received more GST than you’ve paid, then you owe that balance to the IRD. In the reverse scenario, IRD will refund you.

A GST tax report is due after the taxable period on the 28th of the following month. With two exceptions. The taxable period ending on 31 March is due on 7 May, and the taxable period ending on 30 November is is due on 15 January.

Example:

You you need to pay taxes for the period September 1st till October 31st, then your GST deadline is November 28th.

You can file your GST in two ways

-

Via myIR. Simply click on the ‘myIR login’ at the top of the IRD website.

-

Paper forms. You will be sent paper forms if you do not have an myIR account.

—---------

Any tax-related information provided by us is not tax advice, financial advice, accounting advice, or legal advice and cannot be used by you or any other party for the purpose of avoiding tax penalties. You should seek the advice of a tax professional regarding your particular circumstances. We make no claims, promises, or warranties about the accuracy of the information provided herein. Everything included herein is our opinion and not a statement of fact.